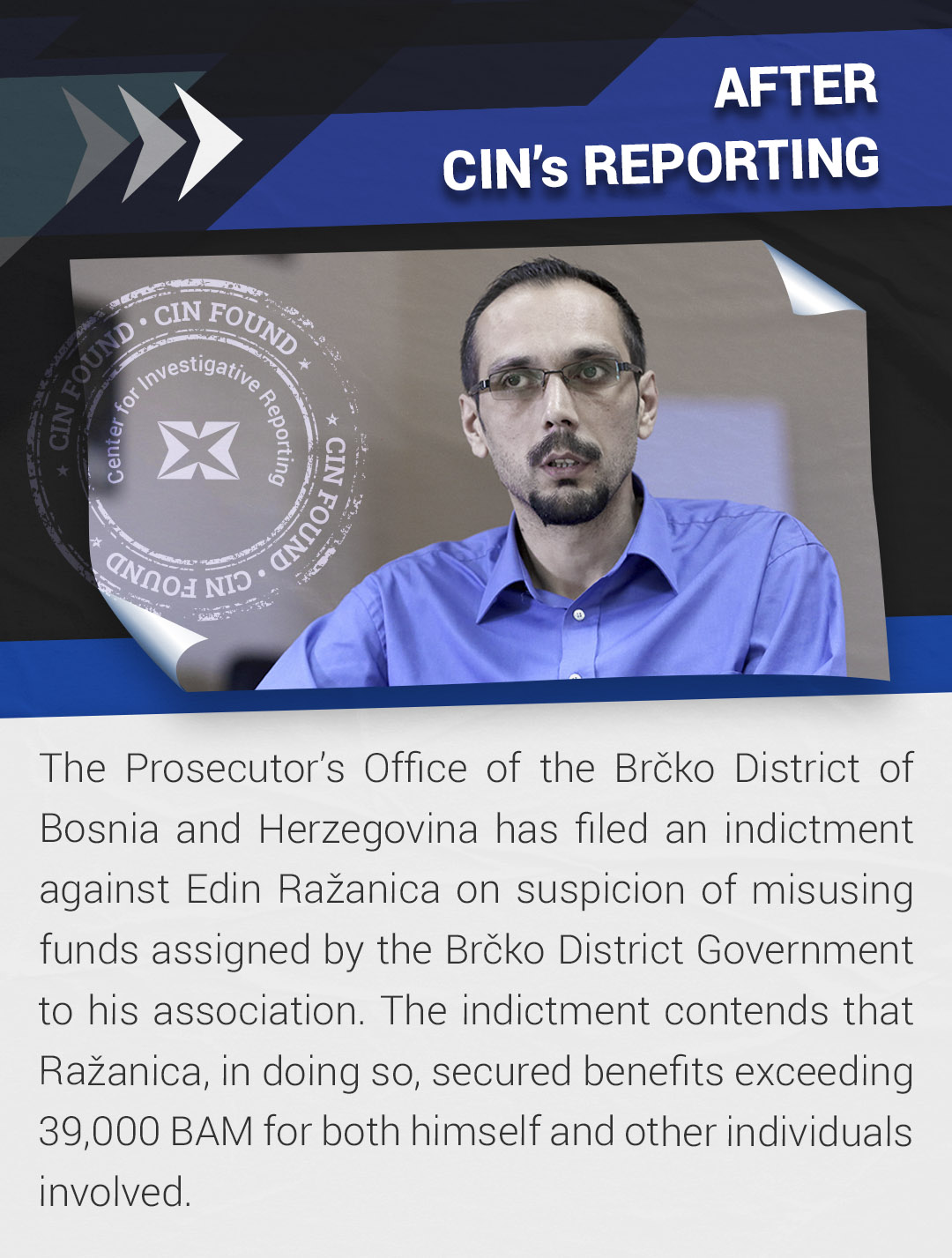

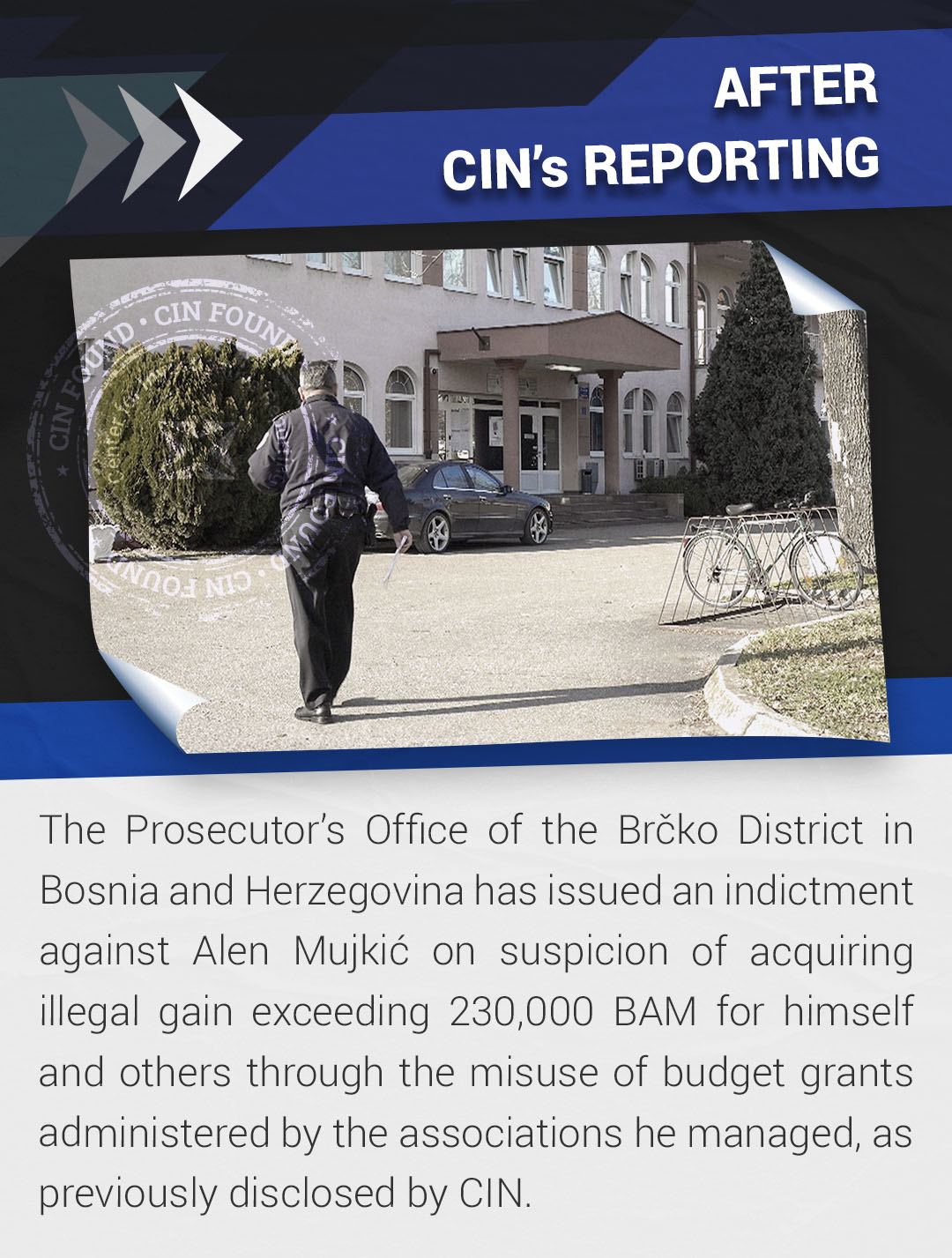

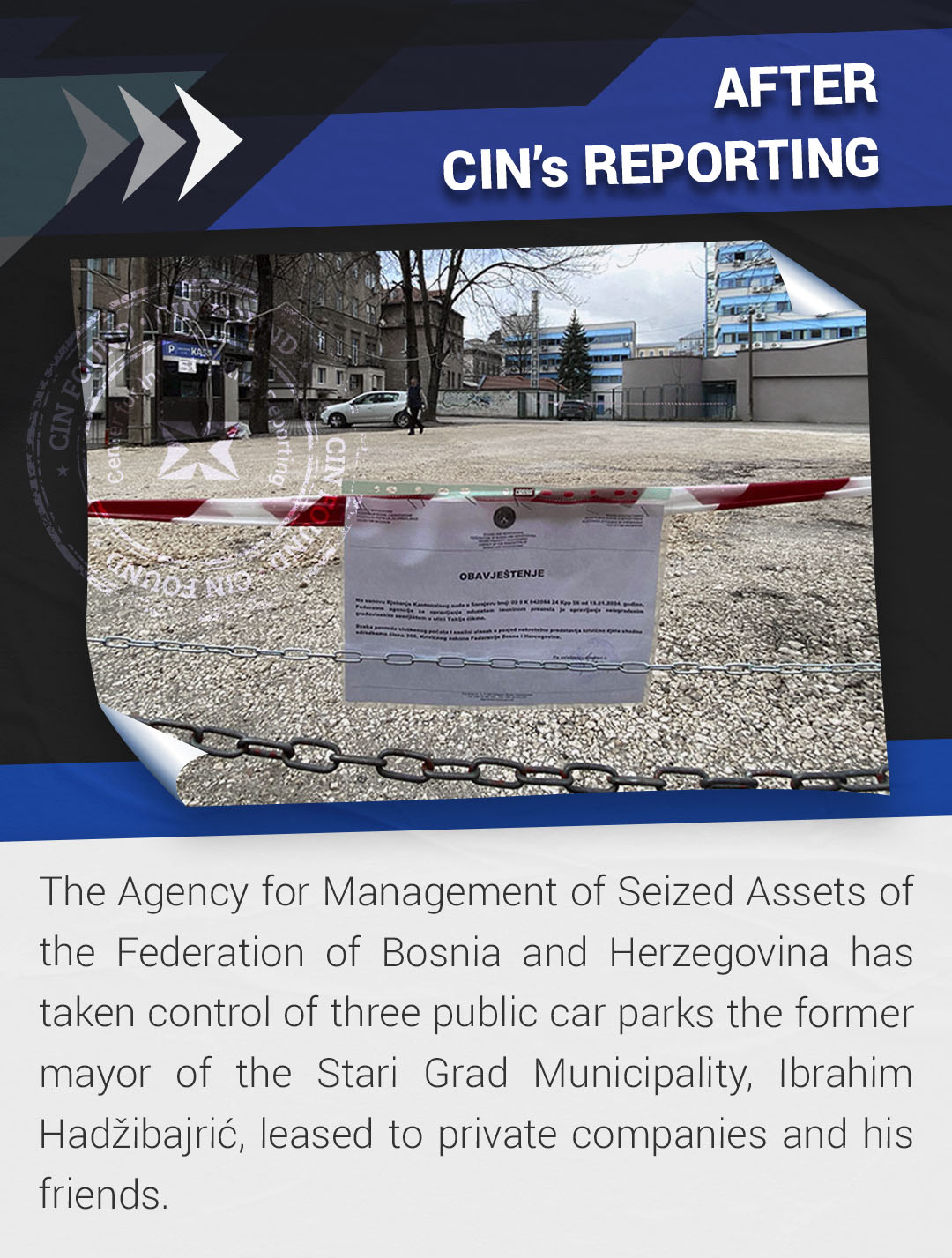

“Come, let’s make a deal!” was the overture to customers on First Bank’s website at the time when it was Montenegro’s second largest bank.

New graft

The bank made lots of deals, mostly with family members, shareholders, business partners and others owners were involved with. Up to two-thirds of loans issued were to parties connected to the bank, according to a never-released draft audit by PricewaterhouseCoopers (PwC) obtained by the Organized Crime and Corruption Reporting Project (OCCRP).

The Central Bank was concerned that too many loans were concentrated in a small group, putting the bank at great risk. Indeed, the bank later got into such a serious financial condition that it required a taxpayer bailout. It was saved only after the government privatized Elektroprivreda, Montenegro’s electricity monopoly. The bank finally became liquid on Sept. 23, 2009, when €192.2 million from that agreement was put into its account.

The PwC based its study on a sample of the top 30 borrowers and nearly 56 percent of the loan portfolio. It is impossible to know the true number of insiders who got loans because First Bank failed to provide auditors with a complete set of documents.

The audit shows that a number of the companies the PwC audit single out as related parties already had raised eyebrows at the Central Bank as early as 2007. It warned that in issuing the loans, the bank was ignoring even its own rules, breaking the law, and damaging the bank for the sake of giving special treatment to VIPs.

Many of the loans were for the lucrative real estate industry. As Aco Djukanovic

Aco Djukanovic

Photo by Vijesti the market collapsed in 2008, many VIPs were unable to make good on debts.

A liquidity crisis forced the bank to seek a bailout in December 2008. But the bank didn’t follow rules or check its free dealing ways even with the public’s money. In some VIP cases, the bank did not seize and sell off the property that had been offered as collateral. In other cases it extended the terms of the loans and grace periods, and allowed deposits intended as loan security to be withdrawn in advance of repayment.

The bank at one time held more than €491 million in depositor’s money, including more than €100 million of government, municipal and public company funds.

Reports from the Central Bank, the primary regulator, show that problems began shortly after the brother of former Prime Minister Milo Djukanovic privatized the bank in November 2006.

Rule no. 1: Know Your Customer (Failed)

Most banks try to gather as much information on new customers as possible. But First Bank already knew many of its high profile patrons.

The law requires banks to monitor transactions and to collect identifying information about customers in order to ensure that accounts are not used for criminal or fraudulent purposes. This is easily done. When opening an account, a customer, whether an individual or a business, must provide up-to-date proof of identity – a company registration or a personal document. The bank also needs enough background information on customers, their field of activity and primary source of income and the reason for the account – in order to be able to detect suspicious transactions.

First Bank violated the rules for dozens of companies and individuals, some of which have known connections with the Djukanovic family, according to a review of Central Bank reports OCCRP obtained.

In 2007, Central Bank examiners found that the bank ignored the rules in opening accounts for a group of companies owned or partnering with Zoran Becirovic, a close friend of the Djukanovics who has represented the country’s trade interests in Russia. The companies, Caldero Trading, Beppler Property and Development, and Beppler Investments, from Cyprus and Beppler and Partners registered in the British Virgin Islands, are in tourism and operate Hotel Avala in Budva and Hotel Bianca in Kolasin, two of Montenegro’s swankiest resorts.

This and other violations triggered a reaction from the Central Bank. On July 6, 2007, First Bank signed an agreement with the regulator pledging to fully comply with Montenegrin money laundering laws. It committed to clean up paperwork on already opened accounts before allowing further transactions.

Four months later, examiners looked into a sample of 48 new companies registered.

The bank did not comply in one significant case and opened an account for the Seychelles-based Camarilla Corporation based on old registration documents.

Up-to-date documents are vital because a company’s situation can change quickly, says Mark Outhwaite, a UK money laundering expert. He said a bank must know where and who its clients are and what they are doing at any time.

The Camarilla Corporation surfaced in the trial against Dusko Saric, brother of fugitive narco-boss Darko Saric, wanted by Interpol for smuggling cocaine from South America to Europe.

Montenegrin prosecutors alleged Dusko Saric and other businessmen laundered at least €7.4 million through accounts at First Bank. He was found guilty.

Subsequent reports found dozens of similar violations, including the case of Lafino Trade, registered in the US state of Delaware. Dusko Saric owns it, according to court testimony.

Outhwaite says banks always face the risk of being used by organized criminals. How seriously they take anti-money laundering law can be indicative of how willing they are to prevent it.

Rule no. 2: Loan Smart (Failed)

The golden years of Montenegro’s economy came in 2006 and 2007 when it ranked as one of the fastest growing non-oil economies in the world. In part, a strong influx of foreign capital was to thank for this, according to a November 2008 World Bank report. During those two years, foreign investors, many of them Russian, bought real-estate valued at more than €850 million. Montenegrins sought a way to profit from demand for Adriatic property. Many rushed to buy parcels or develop property and to get rich quick. But not all of them had their own money or wanted to use their own to invest.

First Bank, privatized by Aco Djukanovic just one month earlier, in December 2006, adopted a strategic plan which called for approving €120 million in loans in 2007. By the end of February it had already reached that milestone, but the bank kept on lending.

In the first report following privatization, Central Bank examiners found that at least one third of the loans they looked at were for the purchase of land or construction of real estate. Many went to companies newly established or with no business plan.

This worried the Central Bank: “The bank has the inadequate practice of granting loans to newly established companies without reviewing the business project for which realization the money is approved, as well as the cash flow for the purpose of constructing residential objects or land purchases.”

There was more to worry bank examiners. The loans came with long grace periods and allowed for a one-time, lump-sum payment.

“Such approval of the long term loans, in addition to the grace periods, is not consistent with sound banking practices.”

Instead, The Central Bank counseled, First Bank should “consider the quality of business ideas, monitor their implementation and release the loan in tranches based on the degree of implementation.”

Milo Djukanovic

Milo Djukanovic

Photo by Vijesti A month-old company, Global Montenegro, received a €3 million loan in February, 2007. Its owner, businessman Vuk Rajkovic, was best man at Milo Djukanovic’s wedding. The money was used to buy land in Budva. One year later, Djukanovic became a partner in the firm—just four days before he returned to the prime minister’s position.

The loan was given on generous terms. Global Montenegro received a three-year loan with a 12-month grace period.

In the July 2007 agreement, the bank pledged to “improve the procedures for approving loans to newly established companies in a sense of defining the terms for approving loans which need to include analyzing the business projects and primary source of repayment.”

However, the bank continued as it had done. On Feb. 13, 2008, the Central Bank issued a formal decision which concluded that the bank had to stop giving unsecured and improper loans.

But this did not deter the bank either.

Instead, the Central bank found that giving loans under these conditions had become unofficial policy of the bank. Rather than a consistent policy towards clients, it would award loans to individuals or business entities “based on personal criteria, affinity or acquaintanceship or some other facts are creating a policy of the bank on a case to case basis.”

Examiners warned that these loans carried greater risk because borrowers had no incentive to pay off: “Loans with greater grace period should be approved only in exceptional cases and such practice of financing should not be common.”

This problem, said the Central Bank, was exacerbated by the fact that the bank did not properly secure loans.

In a Jan. 15, 2009, report, bank examiners found that in many cases the value of property used for collateral involved “deviations from loan policies.”

In particularly worrisome cases, loans secured with collateral were not registered until months after the money had been disbursed.

When assessing property to be used as collateral, First Bank management in some cases did not get professional and independent examinations but just negotiated value with the loan holders themselves. They often settled on the valuation the customer favored. Examiners concluded that neither the process nor the methodology was documented in any way. And it was worrisome given the rapid growth in the real estate market.

“The bank was accepting collaterals in the same value as real-estate,” Milenko Popović, a professor at the Montenegro Business School told OCCRP.

“An asset at a given point is worth €1 million. That is how much it is estimated at. But those values were often grossly exaggerated in a booming market. We had a real-estate bubble.”

If the real estate appraisal values are wrong, it makes it impossible to assess the true value of not only the property but also the bank itself.

Rule no. 3: Follow Up (Failed)

Towards the end of 2008, Montenegro’s real estate market slowed in tandem with the global economic crisis. Few were buying property. The time came for the bank to collect on its loans. But its imprudent loan issuing practices meant many of its customers could not pay.

The Central Bank had repeatedly warned First Bank it needed to more closely monitor the financials of its clients.

This information would separate potentially delinquent clients from highly qualified borrowers and determine a company’s future repayment viability.

On many occasions, the bank did not even verify the self-reported salaries of loan applicants and would grant loans without confirming primary sources of income for individuals or businesses.

A February 2009 report bluntly said that First Bank “is not capable of adequately estimating the credit worthiness of the debtors, i.e. their ability to pay off the loan from their primary sources of income.”

A June 2009 report identified more problems. Examiners sought access to proof of collateral in some cases, but the bank failed to provide evidence that the collateral existed.

In report after report, the Central Bank complained that First Bank had failed to report some loans and guarantees to the Central Bank and the loan registry, which is required by law.

First Bank would report to the credit board, but not until months after it had disbursed loans, noted a May 2010 report.

In still other cases, the Central Bank found that loans granted with specific terms for housing were actually used to other ends like real estate development or construction.

Rule 4: Collect (Failed)

Mark Twain famously said that a banker is someone who gives you a dollar when it is sunny and takes it away when it rains. But this was not true at First Bank. Even as its reserves emptied, the bank restructured loans on favorable terms for clients, not for the bank, mostly by adding extra grace periods.

“The initially poor structure of the loan has significantly resulted in the need for new restructuring in terms of prolonging the deadline or increasing the grace period,” wrote Central Bank examiners in a May 2010 report.

The bank had the highest number of restructured loans of all banks. Over 40 percent of all restructured loans in the country belonged to First Bank.

In some cases, the bank would approve an additional grace period after the original grace period ended, as for example, in the case of Beppler and Jacobson.

In a 2010 report, the bank not only didn’t collect on the loans but actually financed some clients through restructuring, approving an increase in the original amount of the loan instead of penalizing the borrower or claiming the collateral.